Some attention has been devoted in recent years to the matter of blockchain adoption — more specifically, when will blockchain technology go mainstream — and when it does, how will we even know? The question is somewhat problematic because blockchain is an infrastructure, operating in the background — out of sight — that runs across multiple industries and domains.

In an effort to shed some light on this point at issue, Cointegraph Magazine informally surveyed industry thought leaders to complete this sentence, “We will know blockchain has gone mainstream when _______.”

Michael Peshkam, executive in residence at European business school INSEAD, told Cointelegraph Magazine that there were over 50 million Blockchain wallet users at the end of June 2020. “Traditionally this is the number of users [needed] to accept that a technology has gone mainstream.” It took the automobile 62 years to reach the “magic” 50-million-user mark, the telephone 50 years, electricity 46 years, and the internet seven years.

We are in a networked world today, of course, where a technology can spread at an exponential rate — and the world also has many more consumers than in Henry Ford’s time — so it isn’t really fair to compare discrete items like automobiles or telephones to encrypted, distributed digital ledgers. For his part, Peshkam accepts the 50-million-user threshold as a necessary metric, but not a sufficient one. As he explained:

“In my view this number, while a useful indicator, is not sufficient to declare Blockchain is in the mainstream.”

“The missing piece before mass adoption of Blockchain can happen is a simple app with clear value proposition.”

Are numbers even useful?

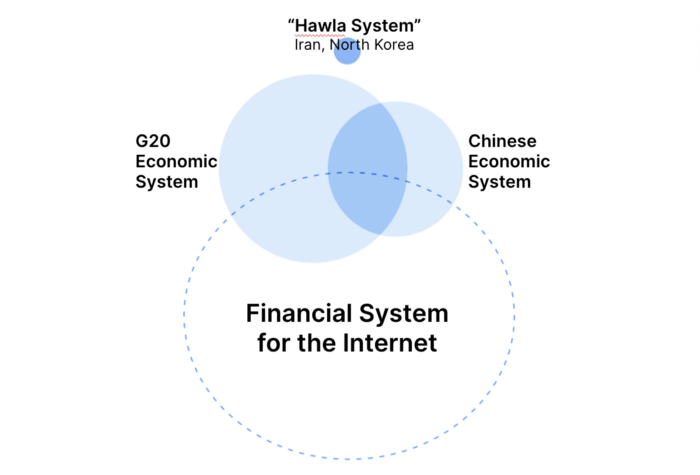

In fact, none of the cognoscenti to whom Cointelegraph posed this question answered with a numeric threshold alone. Garrick Hileman, head of research at Blockchain.com, provided a one line answer: Mass adoption has arrived when “crypto is the financial system for the Internet.”

According to a Blockchain.com blog that expands on this point, the circumstance might look (schematically) something like this:

(Blockchain.com)

But it still begs our question, because how will we actually know when crypto becomes the financial system for the internet? The blog describes Blockchain.com’s goal of reaching 1 billion on-chain crypto wallets by 2030. Presumably, that would indicate mainstream acceptance — but for that to happen, the company concedes, crypto will need to be easier to use, more transaction friendly, and less costly (i.e., lower fees).

Do traditional metrics apply?

Michel Rauchs, the head of Paradigma — a consulting firm focusing on the digital assets sector — as well as a research affiliate and former lead for the cryptocurrency and blockchain research program at the Cambridge Centre for Alternative Finance at the University of Cambridge, told Cointelegraph that traditional metrics for software are only of limited utility.

“For instance, the number of developers or total software downloads doesn’t provide information about the actual impact of the technology. It’s a bit like trying to assess the value of COBOL by merely looking at the number of active developers: it’s still the predominant programming language underpinning much of core banking systems that process trillions of dollars in value, yet there is an acute shortage of developers on the market that are familiar with the decade-old language.”

That said, some additional metrics that might further inform the question asked, in Rauchs’ view were:

- Number of networks deployed (particularly in regard to enterprise distributed ledger technology, or DLT)

- Number and size of direct network participants. Are these small companies or large conglomerates with a global footprint and user base? “Onboarding a large multinational opens up the technology to potentially millions of indirect beneficiaries,” according to Rauchs

- Network value: total value transferred (if applicable), total cost savings, new revenue generation, etc. — “Are we talking about millions or billions of dollars?”

- Availability: Is it natively integrated into major enterprise IT stacks? “We can already see increasing support from major cloud providers for the top-5 enterprise DLT protocols.” said Rauchs.

With regard to cryptocurrency — a sector within the blockchain technology universe — Vili Lehdonvirta, Associate Professor and Senior Research Fellow at the University of Oxford, told Cointelegraph Magazine: “Relative market size doesn’t matter; what matters is the absolute size of the ‘currency area,’ or the set of goods and services that can be purchased with the currency.”

Lehdonvirta is skeptical with respect to Bitcoin, which many think will be the first blockchain technology case to achieve mass adoption, because the crypto community seems willing to move the goalposts to suit its purposes. “When merchants started dropping Bitcoin, enthusiasts changed to other — questionable — definitions of success,” he told us. For example, many now view Bitcoin as a store of value rather than a medium of exchange — which invites different adoption metrics.

A problem must be solved

Geoffrey Moore is author of the book Crossing the Chasm, which builds on the work of Everett Rogers, who first described the five stages through which a technology becomes “diffused” — i.e., goes mainstream: innovators, early adopters, early majority, late majority and laggards. In his book, Moore describes a critical “chasm” that all technologies must cross between the “early adopters” and “early majority” stages if they are ever to achieve mass adoption. He told us:

“Bitcoin [i.e., the most prominent instance of blockchain technology] is still in the early market before the chasm. That is, it attracts customers who ‘believe what we believe.’ But the mainstream market is more skeptical.”

To navigate the chasm, Moore continued, the technology needs to target a market segment of pragmatic customers “who are struggling with an intractable problem that cannot be solved by conventional means.” That use case has yet to emerge, in Moore’s view. With regard to Bitcoin, at least, “valuations are still based on the skewed feedback from an enthusiastic cohort that are focused wholly on the upside.”

Peshkam agrees. Blockchain is here to stay, but it still needs a clear application with tangible benefits for its mass adoption by the public — which he predicts “we are going to see by 2025.” Key areas will be business-to-business supply chain product data, digital wallets for B2B and business-to-consumer transactions/daily shopping as well as blockchain-based health records and personal assets like family trust items and deeds.

Simplicity and ease of use also matter

Campbell Harvey, professor of international business at Duke University, told Cointelegraph Magazine: “Blockchain will be mainstream when people don’t even know they are using the technology.”

Usability will be critical. With the Internet, one recalls, easy-to-use browsers (e.g., Mosaic, Netscape Navigator), were a key innovation leading up to widespread adoption:

“The growth of easy-to-use Web browsers coincided with the growth of the commercial ISP business, with companies like Compuserve bringing increasing numbers of people from outside the scientific community on to the Web – and that was the start of the Web we know today.”

Two main problems are preventing large scale adoption at present, Harvey recounted: scaling and the oracle quandary.

“The main blockchains, Bitcoin and Ethereum, simply do not have the capability in terms of transactions per second (TPS). Visa can do 24,000 TPS while Bitcoin can do about 5 and Ethereum 10. To realize the blockchain dream, even 24,000 TPS is not good enough.”

As for the oracle problem, if blockchain is to succeed, it is necessary to collect information from trusted sources outside of the network, such as a price feed. “This is a challenging problem where a ‘trustless’ blockchain technology needs to trust third-party data,” said Harvey.

Who’s talking now?

One way we may know that blockchain has gone mainstream is when people stop talking about it. As Allen Lee, founder and chief architect at QLC Chain told Zage in a 2019 report:

“I personally believe that the day when blockchain technology is used in day-to-day life is the day when people stopped talking about blockchain. Because it is just a backend technology that consumers don’t need to know about.”

Along these lines, Kevin Werbach, professor of legal studies and business ethics at the University of Pennsylvania’s Wharton School, told Cointelegraph Magazine:

“We will know blockchain has gone mainstream when articles about blockchain-based systems no longer feel the need to highlight the use of distributed ledger technology. No one finds it interesting or surprising today that an application stores data in the cloud, for example.”

Werbach also stressed the need for further regulation, particularly in the case of cryptocurrency. [Werbach, like others, prefers to distinguish between cryptocurrencies and enterprise blockchain.] “We will know cryptocurrency has gone mainstream when [unregulated stablecoin] Tether is no longer a significant source of liquidity for Bitcoin,” he told us. “Crypto will not be mainstream as a financial instrument until it operates within the boundaries of global regulation. Tether’s continued prominence is the best indicator that is not yet the case.”

Waiting for Armageddon

A sizable faction within the cryptoverse views blockchain as a savior technology, one that won’t truly kick in until the current financial system collapses, as it inevitably must under the weight of unsustainable fiat-currency manipulations. “Blockchain doesn’t go mainstream until things in the real world break,” Vinny Lingham, co-founder and CEO of Civic Inc., told Cointelegraph Magazine, because otherwise blockchain is just too much trouble — it’s expensive, not particularly user friendly or intuitive, and it has a steep learning curve. “It’s easier to give my money to a bank,” as long as the status quo prevails. The real world economic order has to break in some manner, and then blockchain can ride to the rescue.

Is COVID-19 the sort of global crisis that could catapult blockchain into the mainstream? “COVID-19 is definitely collapsing parts of the economy,” Lingham answered. It behooves blockchain firms working in these areas to apply their experience and learning to find new solutions, he said.

In the wake of the pandemic, medical records is one area where governments are going to be “extremely paranoid,” suggested Lingham. How can health authorities be really sure that an individual has been vaccinated against COVID-19 and won’t infect dozens of others at a football game, say? Vaccination documents can be faked, but that risk diminishes if vaccinations are certified on a tamper-free blockchain.

Diversity matters too

What about demographics — do those need to be right as well? The history of Internet adoption is instructive. At one point in the 1990s, the average Internet user “was a young professional man with an above-average income.” The internet was still a niche technology, arguably.

It eventually became more inclusive. By 1999, reported e-Commerce Times: “The education level of the user is on par with the general population, as is the income level of today’s user. Older Americans are logging on as well.”

For blockchain technology, would 50% usage by the high-income professional males qualify as “mass adoption” — or do the demographics have to be broader as with the Internet at the end of the 1990s?

Tracking adoption is made more difficult by the vagueness and sometime confusion of the term “blockchain technology.” As Lehdonvirta told Cointelegraph Magazine:

“The problem with measuring ‘blockchain adoption’ is that there is no definition of what ‘blockchain’ actually means, so it could be anything.” Companies like IBM and Microsoft use the term ‘blockchain’ to sell distributed databases, while companies like Guardtime have retroactively branded pre-Bitcoin data integrity products as ‘blockchain.’” Continued Lehdonvirta:

“If all that you need to have to call your system blockchain is a hash chain somewhere under the hood, then most of the world’s major companies probably already use ‘blockchain,’ and it was already mainstream before Bitcoin was even invented.”

‘No magic number’

All in all, we appear to have a problem knowing when blockchain goes mainstream because it is a back-end technology used by many governmental, health, and educational sectors as well as businesses and consumers. As Rauchs told us:

“There is no magic number or threshold that will determine the mainstream adoption of “blockchain,” simply because it’s an industry-agnostic general-purpose information system technology with a wide range of applications in many distinct domains.

At a minimum, it must solve some widespread problem before it will be recognized as mainstream, and with regard to Bitcoin, it has to be more than just a speculative tool. “It has to win adoption as a means of payment for real goods and services, not just for use in crypto speculation,” said Lehdonvirta.

For a significant use case to emerge, however, more technical progress may also be needed. “I am most concerned about the scaling problem,” Duke University’s Harvey told us, “There has been very limited progress.” This has led corporations to implement so-called “permissioned” or even “private” blockchains to achieve higher TPS. These, in turn, erase one of the wonders of this new technology — its trustless aspect, Harvey told us. But once blockchain technology creates a consequential societal enhancement — along the lines of what email did for human communication — then we should know it, even if we can’t quite quantify it.

To borrow from United States Supreme Court Justice Potter Stewart in explaining his definition of obscenity in an Ohio court case — we will know it when we see it.

{kind=link}